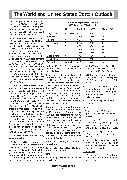

The World and United States Cotton Outlook cated that producers intend to mod- estly reduce ELS cotton area in 2020. USDA’s first survey of producer plant- ing intentions - Prospective Plantings - will be conducted in early March and published on March 31, 2020. For the purposes of this analysis, cot- ton plantings of 12.5 million acres are estimated to result in harvested acre- age of about 11.0 million acres, 7 per- cent below 2019. The projected national abandonment rate of approximately 12.5 percent is based on regional long- run averages, with the exception of the Southwest, where 2020 abandonment is projected at 19 percent—down from 23 percent in 2019. Southwest aban- donment rates are highly variable and conditions there will have a consider- able impact on the U.S. crop. The lat- est NOAA seasonal outlook for the Southwest indicates that drought is not forecast to be an issue through at least the end of April. USDA is forecasting a national aver- age yield - based on regional average yields - of 855 pounds per harvested acre, up from the 2019 yield of 817 pounds. The 2020 U.S. cotton crop is projected at 19.5 million bales, 3 per- cent (600,000 bales) below 2019, as a rebound in the U.S. yield offsets much of the area reduction in 2020. Smaller crops are anticipated for most of the Cotton Belt, with the exception of the Southwest, where 2020 cotton produc- tion could rise to its second highest on record. Based on higher U.S. carry- in stocks of 5.4 million bales for 2020/ 21 but lower production, the total sup- ply - 24.9 million bales - would nearly match that from 2019/20, which was the highest since 2007/08. U.S. Disappearance, Ending Stocks, and Farm Price U.S. domestic mill use is projected at 3.0 million bales, essentially un- changed from 2019/20, due to contin- ued import competition and moderate growth in domestic demand. U.S. cot- ton mill use will also be sustained by a rebound in semi-processed textile and apparel exports—mainly to MexicoU.S. Cotton Supply and Demand 2019/20 est. and 2020/21 proj. Unit2019/202020/21Change (%) Beg. Stocks ProductionMil. bales "4.85 20.105.40 19.5011.3 3.0 Imports Total supply" "0.01 24.960.01 24.910.0 -0.2 Mill use Exports" "3.00 16.503.00 16.500.0 0.0 Total use Ending stocks" "19.50 5.4019.50 5.300.0 -1.9 Stocks-to-use Farm price% cents/lb.27.7 62.027.2 64.0-1.8 3.2 and the CAFTA-DR/CBI countries— that are finished and shipped back to the United States.•894,000 metric tons (MT) TRQ at 1% duty; calendar year basis, one- third reserved for State Enterprises. Exports are projected unchanged at 16.5 million bales, reflecting in part the stability of U.S. exportable supply. China’s rising imports and easing U.S.- China trade tensions are favorable for U.S. exports to some degree, but Bra- zilian exports are expected to remain near record levels and the United States will face additional competition early in the season as India’s remain- ing priceintervention stocks become available to world markets.•Sliding scale impor t licenses, 800,000 MT issued; valid Sept/18- Feb/19, but licenses were not fully used. •Imports of U.S. cotton faced addi- tional 25% duty starting in June; some imports by State Enterprises and for processing exempt from additional duties. •Imports of foreign cotton by State Reserve. Ending stocks are projected to decline slightly, their first decline in 4 years. At 5.3 million bales, U.S. ending stocks in 2020/21 are expected to be 100,000 bales lower than during the year be- fore. Reduced stocks in the United States and in other countries outside of China are expected to reduce pres- sure on cotton prices in 2020/21, and the average price received by produc- ers could rise to 64 cents per pound, compared with the 2019/20 current fore- cast of 62 cents.2019 China Cotton Policy and USDA As- sumptions• Out-of-quota duty, TRQ, and duty-free processing imports same as previ- ous year. •Imports of U.S. cotton face addi- tional 25% duty; some imports by State Enterprises and for process- ing exempt from additional duties. •Imports of foreign cotton by State Reserve, but U.S. imports ex- cluded. •Additional access provided; addi- tional Sliding Scale quota of 800,000 tons issued, but licenses were not fully used.Import Policy: Sliding Scale Quota Is- sued Starting in 2018 2020 & 2021 2018 • •Out-of-quota import duty is 40% ad valorem. NCM-MARCH 2020 31Out-of-quota duty, TRQ, and duty- free processing imports same as previous year.