By which measures for the prevention and control of customs fraud are adopted in the imports of fibers, yarns, fabrics, clothing and footwear.

THE PRESIDENT OF THE COLOMBIAN REPUBLIC

In exercise of its constitutional and legal powers in particular which it is given on numerals 11 and 25 of article 189 of the Constitution, the laws 7, of 1991, 1609 of 2013, 1762 of 2015, heard by the Committee of Customs Affairs, Tariff and foreign trade, and

WHEREAS

That in some cases, foreign trade operations are being used by criminals to launder money, finance terrorism and generate organizations unfair competition by entering into the country contraband goods.

That these behaviors generate a negative and harmful impact on the industry and the trade sector having to confront distortions in prices and compete in inequitable conditions with organizations which evade the payment of customs taxes among others.

That one of the methods used by criminal organizations is making imports using customs fraud practices.

That the sectors of fiber, yarn, textiles, clothing and footwear have been affected significantly since their characteristics make them attractive for criminal organizations laundering assets and other illicit, by its high rotation and for being generic goods of massive consumption.

That taking into account of such conduct, threats to the ‘ stability economic sector and the impact on Customs and tax revenues, it is necessary to implement new mechanisms that allow to control and to counteract this scourge.

That the inter-institutional Commission of fight against smuggling in extraordinary session performed on August 24, 2016 recommended the adoption of the strategies referred to in this Decree.

The customs affairs Committee, tariff and International trade in its 307 session of November 10, 2017, recommended the adoption of measures incorporated in this Decree.

The special economic and trade conditions above requires the adoption of urgent measures, reason why it is necessary to give effect to the exception contained in paragraph 2 of article 2 of Law, 1609 of 2013.

Continuation of the Decree “By which measures for the prevention and control of customs fraud are adopted in the imports of fibers, yarns, fabrics, clothing and footwear”

That complied with the formalities provided for in numeral 8, article 8 of the Administrative procedure Code and of the contentious administrative, in relation to the publication of the present Decree text.

ENACT

Article 1. Object. This Decree establishes mechanisms for strengthen the risk management system and Customs control against possible cases of customs fraud associated with imports of fibers, yarns, fabrics, clothing and footwear, regardless of the country of origin and/or source:

Article 2°. Scope. ( Imports of products consisting of fibers, yarns, fabrics, clothing and footwear in chapters 52, 53, 54, 55, 56, 58, 59, 60, 61, 62, 63 and 64 of the customs tariff, whose price FOB”) declared is less or equal to the threshold established in article 30 of this Decree, shall be subject to measures referred to here.

Article 3°. Thresholds to strengthen risk management and control system customs. Measures referred to in this Decree shall apply to the imported goods whose declared FOB price is less than or equal to the threshold that is determined for the following headings and subheading tariff:

Yarn

Customs clearance number

ThresholdUSD/KG

5205

2.00

5402

2.00

5509

2.00

5510

2.00

Fibers

Customs clearance number

Threshold USD/KG

5503

1.00

5504

1.00

5505

1.00

5506

1.00

5507

1.00

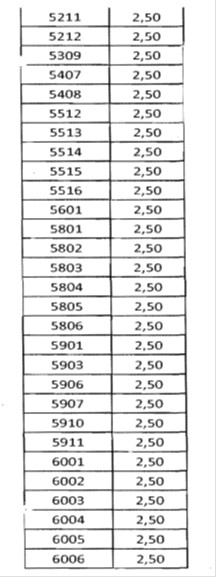

Fabrics

Customs clearance number

Threshold

USD/KG

5208

2.50

5209

2.50

5210

2.50

Continuation of the Decree “By which measures for the prevention and control of customs fraud are adopted in the imports of fibers, yarns, fabrics, clothing and footwear”

Clothing

Customs clearance number

Threshold

USD/Kg

6101

10.0

6102

10.0

6103

5.0

6104

8.0

6105

5.0

6106

5.0

6107

j 5.0

6108

5.0

6109

5.0

6110

8.0

6111

5.0

6112

8.0

6113

10.0

6114

10.0

6115

5.0

6116

5.0

6117

5.0

6201

10.0

6202

10.0

6203

5.0

6204

5.0

6205

10.0

6206

8.0

6207

5.0

6208

5.0

6209

5.0

6210

8.0

621 1

10.0

6212

5.0

6213

5.0

6214

5.0

6215

5.0

6216

5.0

6217

5.0

Made-up textiles

Customs clearance number

Threshold

USD/KG

6301

2,0

6302

2.0

6303

1.5

6304

4.5

Footwear

Customs clearance number

Threshold USD/pair

6401

3.0

6402

3.0

6403

8.0

6404

3.0

6405

4.0

Paragraph. The national Government will review the thresholds laid down in the present article, annually or in a lower term when the dynamics of foreign trade thus warrants it.

Continuation of the Decree “By which measures for the prevention and control of customs fraud are adopted in the imports of fibers, yarns, fabrics, clothing and footwear”

Article40,Import. Natural or legal persons intending to import to the national customs territory and/or introducing EPZ goods from overseas consisting of fibers, yarns, fabrics, clothing and footwear classified in subheadings of the customs tariff listed in article 3 of this Decree, to a lower price or equal to the threshold determined in said article, they must prove to the Customs operation management Division or whoever is in charge, from the Directorate of customs or tax and customs with jurisdiction at the place of arrival, the following requirements:

without prejudice to the submission of the statement on the terms and form established by the Directorate of national taxes and customs, the importer, who must be the same consignee, at least within a month of prior to arrival of goods at the national customs territory must submit for each shipment, the format of identification and responsibility for the terms and conditions that the Directorate of national taxes determines, accompanied of the following documents:

a.) Apostille or legalized with official translation provider abroad, certification to Spanish language in which it shows that it intends to sell to the importer in Colombia, noting in addition, if it is the case, the type of economic bonding with the importer in accordance with provisions in the tax statute, additionally indicating the supplier´s address, telephone, and email address and the subheading tariff to six (6) digits, containing the detailed description of the products that will be exported, the quantity and its respective price.

b) Apostille or legalized certification with official translation into Spanish language in which it points out the existence of the company abroad, which shall be issued by the entity in the country of export who keep the official record of producers or In the case of non-existence of this entity, the importer must manifest such a case under oath, that it is understood provided with the signing of the document, without prejudice to the powers of control and supervision of the Directorate of National taxes and customs.

c) If whoever imports the merchandise will sell it in the same State, shall submit the relationship with distributors of goods in Colombia indicating its NIT, Legal Entity, address, Telephone and e-mail.

d) Written support signed by the legal representative of the Agency of Colombia customs goods, indicating its NIT, company name, address, telephone and email, whenever is needed, in which certifies that they made study of customer knowledge to the importer for whom will do the proceeding with Customs Agency and time schedules relationship between the parties.

e) Written support signed by the importer or importer´s legal representative, which certifies:

That the value to declare of goods subject to import corresponds real paid price or price to pay.

Address of warehouses where goods subject to import are to be storage.

Detailed information of distribution and marketing chain of goods in Colombia subject to import.

That has knowledge of the customs authority Faculty to send to the Colombian Attorney General and to the information department and Financial Analysis – UIAF – documents related to the import´s operation.

Notwithstanding the presence of the Customs Agency representative, when acting through this entity, the importer, the legal representative or agent of the partnership must be present at the examination of Customs inspection or seating of goods.

For these purposes, the importer´s agent must be different to the Customs Agency.

The absence of the importer, the legal representative or the importer agent, will result in no-source or no authorization of release,

Paragraph 1 °. The format of identification and responsibility and designated documents in this article constitute support of the import declaration documents.

The non-filing or untimely file of these documents shall give rise to the not provenance or non-authorization of release.

Paragraph 2′. In the case of goods which they intend to import from a free zone to the rest of the national customs territory, the importer must correspond to the consignee appearing on the shipping document with which he entered the merchandise to the Free Zone, except in the case of products classified under subheading 6406100000, consigned to an industrial user of goods or of goods and services.

In the event that the consignee does not match with the importer will lead to non-origin, or non-authorization of release.

Paragraph 3. They are exclude of the special measures provided for in this Decree, the goods referred to in article 3 of the same, owned by foreign companies or persons without residence in the country, which have been introduced from abroad to Distribution centers logistics international, to be distributed in its entirety to the rest of the world.

Article 5°. Incoming Controls. According to the criteria of the management of risk system, the special Administrative Unit Department of Taxes and Colombia Customs – DIAN may establish customs controls at the entry of the goods, which reference this Decree. If it may establish limitation of income measures, these must be duly supported and justified in accordance with the analysis and technical concept derived from the same risk management system.

Article 6°. Import Monitoring. The Colombian Administrative Unit Department of Taxes and Colombia Customs will provide observers in the import the information that will be provided established by such entity through resolution, which must be issued within sixty (60) calendar days following the effective date of this Decree; such resolution will also establish the procedure for the delivery of information to the observer.

Continuation of the Decree “By which measures for the prevention and control of customs fraud are adopted in the imports of fibers, yarns, fabrics, clothing and footwear”

The observer shall provide cooperation and collaboration required by the customs authority including the technical report as appropriate on classification, identification, quantity, description, weight and price of the commodity among others.

For the purposes of this Decree, the role of the observer shall be limited to analyzing the information and generate alerts to the customs authority, as well as to closely observe the development of the diligence inspection or capacity of goods corresponding to headings referred to in article 3 of this Decree.

The customs authority must safeguard the reserve’s confidential information taking into account the stipulated in the Constitution and the laws 863 of 2003 and 1712 of 2014 and other rules that modify them or complement them.

Article 7 °. Warranty. In the case of goods covered by the scope of implementation of this Decree, if controversy of value is generated as to the inspection diligence or capacity and for this reason it is necessary to take the final determination of the customs value of the same, in accordance with article 13 of the agreement of assessment in customs by the world trade Organization, the importer may obtain release constituting a guarantee sufficient to ensure payment of the customs taxes, penalties and interest to be place.

Warranty will be awarded on a value equal to the two hundred percent (200%) of the difference between the declared FOB price by the importer and the result of multiplying the unit price of the threshold established in article 3 of the this decree by the imported amount.

Warranty shall be from a Bank or insurance company. There will be no place to the security in the form of monetary deposit.

The term of the warranty period shall be three (3) years.

The fact of having constituted a global warranty or not being obligated to provide one, it shall not relieve the importer of the obligation indicated.

Once awarded the release, the Customs operation Management Division or whoever is responsible shall send the Management Division of submission copies of the import Declaration, documents support, warranty and certificate of inspection, related to its jurisdiction.

Article 8 °. Risk management. Importers who declare goods consisting of fibers, yarns, fabrics, clothing and footwear classified in the headings and subheadings of the customs tariff referred to in article 3 of the this Decree, at a price not exceeding the given thresholds in this article, must be reported to the Department of management of operational analysis of the Directorate of national taxes and customs for the purpose of incorporating the information of these operations to the risk management system.

Article 9 °. Transshipment. Not applicable the transshipment referred to in article 140 of the 390 Decree 2016, goods referred to in article 3 ° and which do not comply with the requirements laid down in article 4 of the present Decree.

Article 10 °. Seizure and confiscation. If the developments of performances of customs control are goods covered by article 3 ° of this Decree, shipped subsequent to the entry into force of the same without the fulfillment of all the requirements here provided, shall be subject to seizure.

Continuation of the Decree “By which measures for the prevention and control of customs fraud are adopted in the imports of fibers, yarns, fabrics, clothing and footwear”

PARAGRAPH: The merchandise apprehended stated in this Decree, for any circumstances may be subject to legalization or rescue.

Article 11°. Non-regulated aspects. Whatever is not contemplated in this Decree are to be governed by the provisions of decrees 2685 of 1999 and 390 of 2016 as appropriate.

Article 12°. Effective date and revocation. This Decree comes into force from its publication date in the official journal and repeals Decree 1745 of 2016.

The provisions here adopted, shall not apply to imports of goods that, at the date of entry into force of this Decree, they are effectively shipped to Colombia based on the date of the transport document or they are primary zone customs or in free zone, provided that they are subject to the modality of ordinary import in a period not exceeding twenty (20) days from the date of entry into force of this Decree.

Clothing

Clothing